Optimism

What a nice way to begin this quarterly update. It may be that the darkest days of the pandemic are behind us. There are vaccines inoculating individuals around the world. There is promise that social, personal, and face-to-face activities may be on the horizon.

Our policymakers have kept aggressive fiscal and monetary support intact. This has allowed the US economy to march higher in the quarter as it continues its impressive rebound from the severe recession brought on by pandemic-related lockdowns. This rebound has been further reinforced by the recently enacted American Rescue Plan. This $1.9 trillion fiscal stimulus package is expected to keep the recovery’s momentum going.

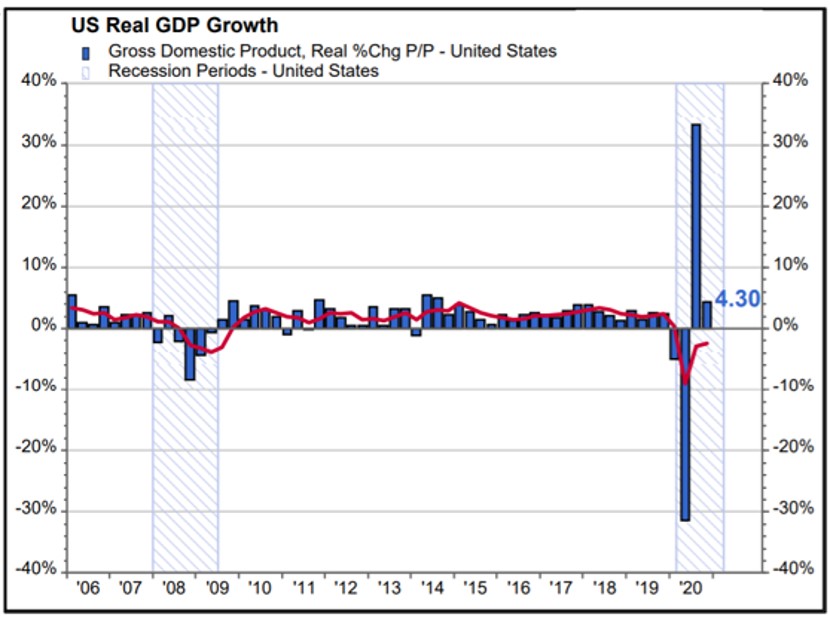

The Bureau of Economic Analysis’ third estimate of the fourth quarter 2020 real GDP was a seasonally adjusted annualized increase of 4.3%, slightly better than the prior estimate of an increase of 4.1%, but significantly lower than the record-setting 33.4% increase in the prior quarter. This is understandable given the deep hole the economy was digging itself out of in the third quarter.

Now the US economy and the global economy are poised for a synchronized recovery.

Morgan Stanley notes in its global economic forecast published in December that all regions of the world are projected to see improvements from the pandemic driven dive they took in 2020. They further note how extraordinary it is for world economies to move in lockstep. Their prediction is for a 6.4% increase in global gross domestic product with the US likely to achieve nearly 6%. The International Monetary Fund recently increased its global outlook to 6% as well.

Perhaps, the best summary of today’s situation and opportunities arising in the future was provided by the leader of America’s biggest bank, JP Morgan’s Chief Executive Officer Jamie Dimon. In his much read and anticipated annual letter to shareholders, Mr. Dimon shared his optimism. A hefty read at better than 60 pages, he suggests that the US economy was emerging from the coronavirus pandemic into a Boom that could last until 2023. He acknowledged that strong consumer saving and expanded vaccine distribution coupled with the potential Biden administration’s proposed $2.3 trillion infrastructure plan could lead to an economic Goldilocks moment- fast sustained growth alongside slowly rising inflation and interest rates.

This growth is expected as we begin to travel a new road ahead, a path that has not been traveled during most of our lifetimes. We will have to monitor and react appropriately as services re-open, employment continues to grow, and overall activity improves—and while consumers begin to spend again. Ultimately it will be the efficacy of the vaccine rollout that is most crucial to the trajectory of the recovery. Even though the number of cases of the virus have declined throughout the world, economists are worried that new variants of the virus or hiccups in the vaccine rollout process could spell a setback for the recovery. In addition, vaccinations will have a significant impact on how quickly mobility—and, by extension employment–will return to normal.

Let’s take a moment to shift from looking forward to glance back at the results from the first quarter.

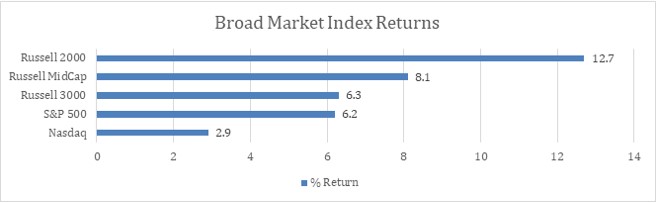

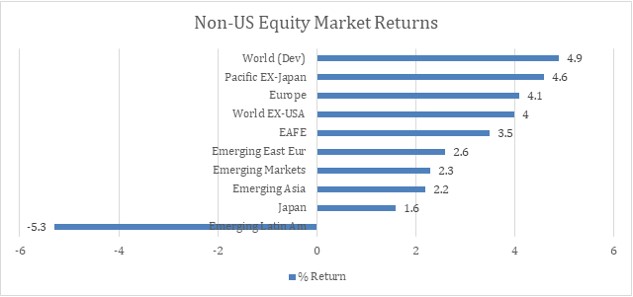

Stocks posted a fourth consecutive quarter of strong gains following the sell-off in the first quarter of 2020. Returns on broad equity market indices were choppy throughout the quarter, but the trend was higher. When the first quarter ended, the S&P 500 Index had advanced 6.2% and has gained 56.4% over the past 12 months. The Russell 1000 Index of large capitalization stocks generated a 5.9% total return. Small cap stocks, as represented by the Russell 2000 Index, outperformed large caps, and finished the quarter with a total return of 12.7%. The NASDAQ Composite, dominated by information technology stocks, finished the quarter with a gain of 3.0%. The Dow Jones Industrial Average of 30 large industrial companies advanced 8.3%. International stocks also generated material gains during the quarter, and generally performed in line with US equities. The MSCI ACWI Ex-USA Index, which measures performance of world markets outside the US, rose by 3.5%. The MSCI EAFE Index of developed markets stocks advanced 3.5%. Regional performance was mixed for the quarter. The Pacific ex-Japan region was the strongest performer on a relative basis, with a return of 4.6%. Latin America was the poorest relative performer, declining 5.3%. Emerging markets performance was modestly positive, as the MSCI Emerging Markets Index was higher by 2.3%.

Coincidentally, it was not only in Washington DC where a change in leadership happened in early 2021.

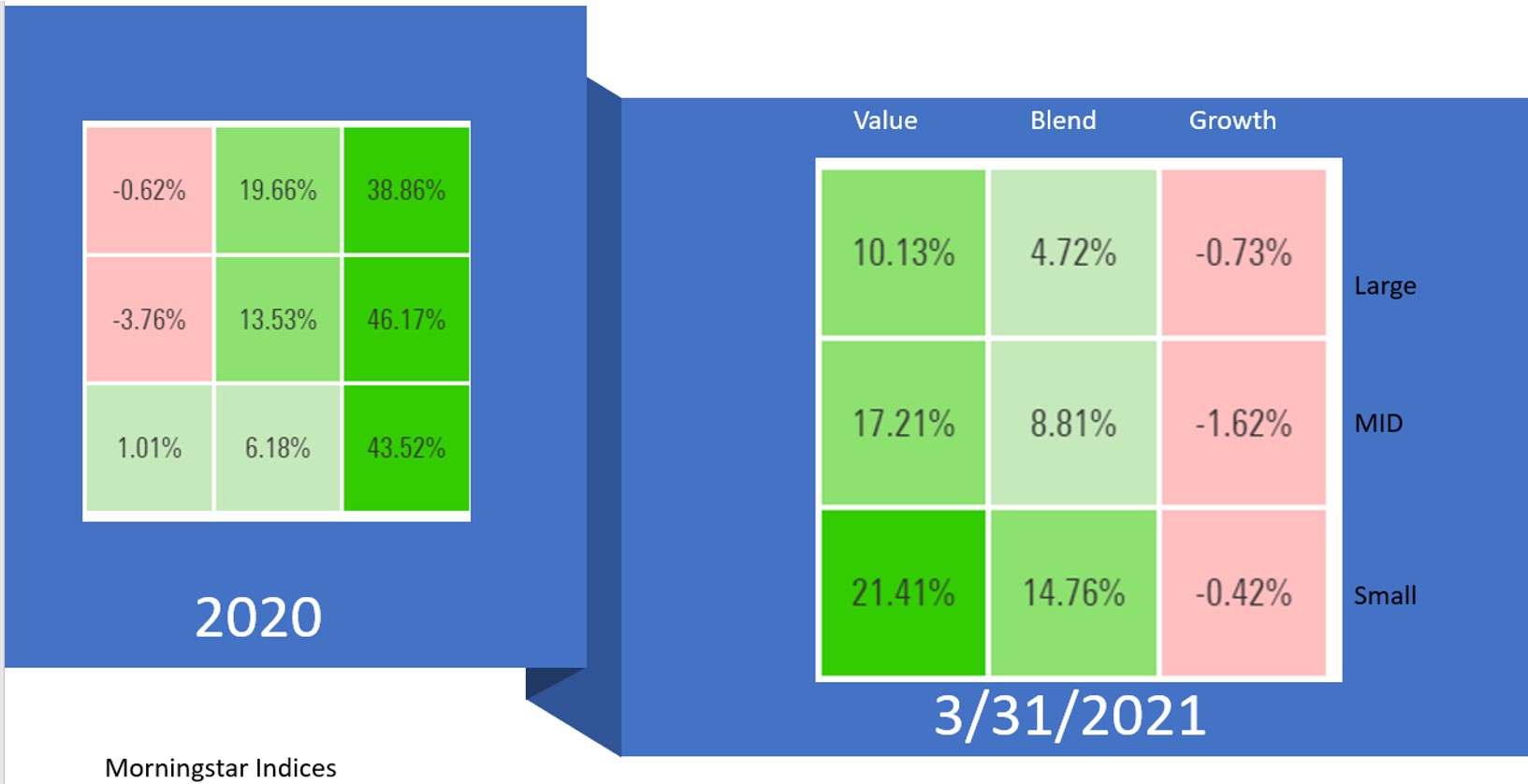

What a difference a year makes. With the new outlook for the economy, investment classes and sectors that had struggled and lagged in performance turned their fortunes around and (finally) achieved stellar performances. Similarly, last year’s achievers cooled down from their red-hot growth. The lagging value stocks leapt to the front while growth stocks faded. Morningstar has prepared the following comparison utilizing their market indices. The vertical axis shows the market capitalization of the respective index. Small caps have capitalization beneath $2.5 Billion; Mid cap measures $2.5 billion – $15 Billion; and large cap stocks are in excess of $15 billion. The horizontal axis shows the investment style (value, blend, or growth).

Performance of each of the eleven primary economic sectors was positive during the quarter, with the more cyclical sectors posting higher returns as the economy accelerated. Energy, Financials, and Industrials were the strongest performers on a relative basis, generating returns of 30.9%, 16%, and 11.4%, respectively. The Consumer Staples, Information Technology, and Utilities sectors were the poorest relative performers posting returns of 1.2%, 2%, and 2.8% respectively.

2020 will be remembered as the year of the pandemic.

From an economic perspective, 2020 was one of the most difficult years in US history, with the economy contracting by 2.4%. 2021 will hopefully be remembered as the year of the recovery. We are hopeful that the economy will continue to open up, and prospects for 2021 will be even more promising than they appear right now.