“The 99.5% Act” was recently introduced to the Senate. If enacted, “the Act” will reduce many existing estate planning opportunities that can protect hard-earned assets.

Do you know how this impacts you and your family?

The time to make use of the current estate and gift tax laws may be running out. If enacted, it could:

- Reduce estate and gift tax exemptions and exclusions

- Reduce the estate tax exemption to $3.5 million

- Reduce the gift tax exemption to $1 million

- Increase the estate and gift tax rate to a minimum of 45% and maximum of 65%

- Limit the annual gift tax exclusion with respect to certain transfers to $10,000 per transferee with a total annual limit per transferor of $20,000, both indexed for inflation (currently would be $15,000 and $30,000, respectively, inflation adjusted)

- Eliminate marketability valuation discounts on passive assets and minority interest valuation discounts on family-controlled business entities

Trust implications

- Impact the Generation Skipping Transfer laws to include a 50-year deemed term for trusts that would otherwise be “generation skipping tax exempt” ·

- Impose a minimum term on Grantor Retained Annuity Trusts of 10 years and minimum remainder value (gift) of 25% of the contribution to the GRAT ·

- Introduce a new Code Section, IRC Section 2901, which would impose a gift tax or an estate tax on property owned by grantor trusts upon termination of grantor trust status during life or at the grantor’s death

There will be complexities associated with these changes. “The Act” reflects anticipated changes to the estate and gift tax laws.

Getting Started

If you would like to understand how the Act could impact you and your family, please call us at 877.536.1014.

________________________

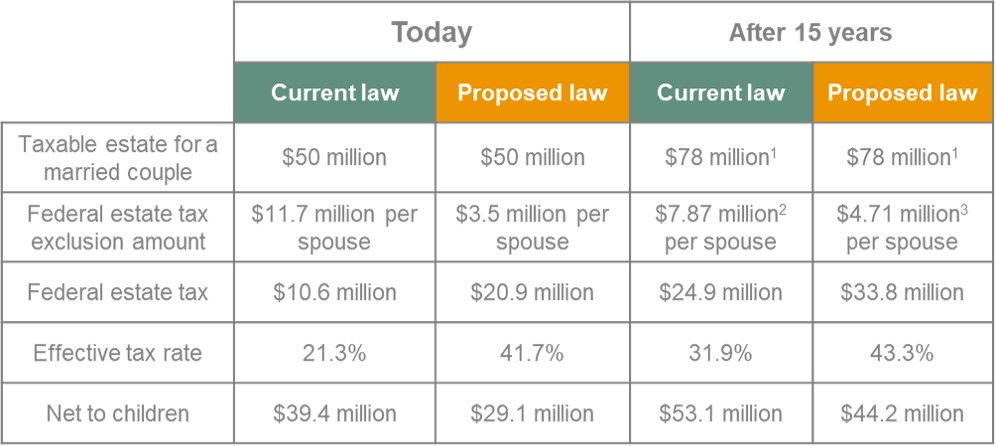

1Assumes the taxable estate appreciates at a rate of 3% per year.

2Assumes an inflation rate of 2% per year and the tax rates and Federal Exclusion Amount in effect under Current law which sunsets after 2025 and the Exclusion Amount reverts to $5 million indexed for inflation.

3Assumes an inflation rate of 2% per year and the tax rates and Federal Exclusion Amount proposed within the 99.5% Act.

SFI Advisors does not provide tax or legal advice. Taxpayers should seek such advice from a tax or legal professional.

Source: Lions Street